The stock market is no exception. Everyone loves a good bargain. While buying items on sale is easy, getting shares at a discount is more difficult.

That’s because a cheap stock often means that it has been through the wringer, and the immediate question that comes to mind is, why have the shares taken a beating?

A stock that has been beaten down may be down due to many different reasons. They could range from fundamental weakness to macroeconomic concerns to investors’ unreasonable behavior. As the saying goes: the trick to buying the dip is to identify the names that have temporarily fallen and will soon rise again.

How can you find these deals? Wall Street experts could be of help. It is their job to determine which stocks are most profitable at any particular time.

With this as backdrop, we opened the TipRanks database to get the lowdown on two stocks that have witnessed a big drop recently, but which certain Street analysts are recommending investors participate in the time-honored act of “buying the dip” ahead of an anticipated rise. The details are below.

Roblox CorporationRBLX)

We’ll start with a look at a gaming and metaverse company, Roblox. Roblox has been around since the early 2000s, offering users an interactive platform to create, play, and share games – and to interact with each other through them. Roblox calls itself a metaverse, offering its users a more immersive online experience than is possible with other companies. The company has combined gaming with community building to encourage creativity and positive relationships among its users.

Some numbers will give the scale of Roblox’s operations. Roblox had 65.5 million average daily users at the end of Q2 of this year. They spent collectively more than 14 billions hours on the platform. This huge user base makes Roblox one of the world’s top platforms for the under-18 audience. The company’s popularity with its target user base is attributed to its ability develop a community among users and developers.

Roblox’s recent 2Q23 results showed that the company had increased its top line. The revenues came in at $680. 8 million, which is a 15% increase year-over-year.

Other results weren’t as good. The net loss per share of 46 cents was a significant decrease from the 30 cents in 2Q22 but still 2 cents more than expected. The company generated $38 million of adjusted net EBITDA. It also reported $780.7 millions in bookings. This is an upward-looking number that’s well above $639.9 from the prior quarter.

The results did not meet analyst expectations. The analysts expected EBITDA at $46m and bookings of $785m. RBLX shares have fallen 23% in the last month after the earnings announcement.

For Wedbush analyst Nick McKay, the key points here are Roblox’s strong position and user base, combined with a lowered price that gives investors an attractive entry point. McKay writes of Roblox, “Q2:23 results brought light to some soft spots within the company, but we think that the data trackers, seasonality, and stubbornness contributed to the misses. Roblox, on the whole, may have the most compelling trajectory for growth among video game names that we cover, taking into consideration its user base, its new products and its potential to revisit its profit approach.

“With Roblox shares trading well below our price target after a selloff, the risk/reward profile has become favorable to the upside… We expect patient investors to be rewarded by continued topline growth coming from the expansion of key user metrics, a slew of new product introductions, and a more aggressive approach to cost control in future periods,” McKay went on to add.

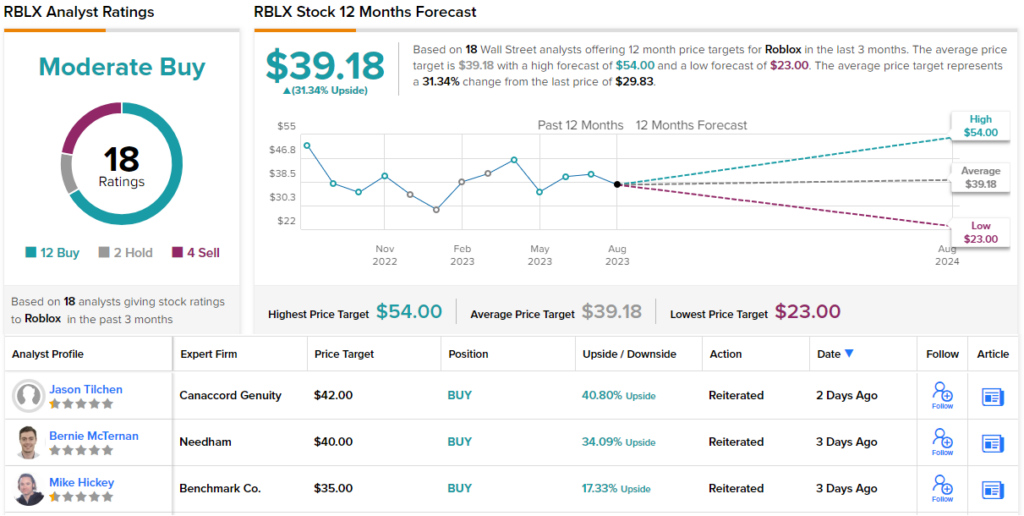

McKay’s rating for RBLX is Outperform (a buy), with a price target of $37, implying an annual gain of 24%. (To watch McKay’s track record, click here)

Street analysts have also adopted a bullish outlook on Roblox. Out of 18 analyst reviews, 12 were Buys, while 2 were Holds. A Moderate Buy consensus was reached. The average price target of $39.05 and the $29.83 current trading price give a combined 31% increase for the upcoming year. (See Roblox stock forecast)

Kornit Digital (KRNT)

Kornit Digital is next, bringing high tech and textiles to the forefront. It is also a producer of pigments and chemical products. These are used in a range of textile industries, including garments, apparel, home goods, and decorating; Kornit’s printing machines can translate complex designs from the computer directly onto the fabric and the finished fabric products, allowing textile workers to call up patterned products on demand.

Textile artists, makers and factories can streamline operations by creating patterned products on demand. They are able to reduce their inventory, eliminate redundancies and free up space. Kornit’s customers can use the technology to support direct-to-garment solutions for a more sustainable fashion industry, that generates less waste and overproduction, and produces a seamless experience to ensure that customers will return.

Kornit has a dominant position in the niche it serves, yet its stock price is down by 27% this month. The company’s losses have come in the days after its August 9 release of the 2Q23 financial numbers. Kornit has posted net-negative earnings for six quarters in a row, but the non-GAAP 15 cent loss per share is 6 cents higher than was expected. At the top line, the company’s revenues disappointed, coming in at $56.2 million, down 3.3% y/y and more than $550 million below the forecast. The revenue miss fed into the share price drop as did a forward 2H revenue guide that came in 7% below Wall Street’s forecast.

When it’s all said and down, Morgan Stanley analyst Erik Woodring believes that Kornit’s share price loss is investors’ gain, as it opens up the stock for opportunistic buying. Woodring takes note of the headwinds, but states that the company has plenty of room for growth, writing, “We are looking past the near-term challenges to what we believe should still be a year of robust growth in 2024, and continue to forecast high 20% Y/Y revenue growth in CY24 (+26% Y/Y vs. +28% Y/Y previously), albeit off a lower 2023 starting base. At a 3.0x target EV/Sales multiple, we are implying KRNT’s shares still trade at a slight discount to its 2015-2019 valuation when the company was compounding revenue at double digits given the risks associated with the weak near-term spending environment. Together, these factors ergeben [are] driving our upgrade to Overweight.”

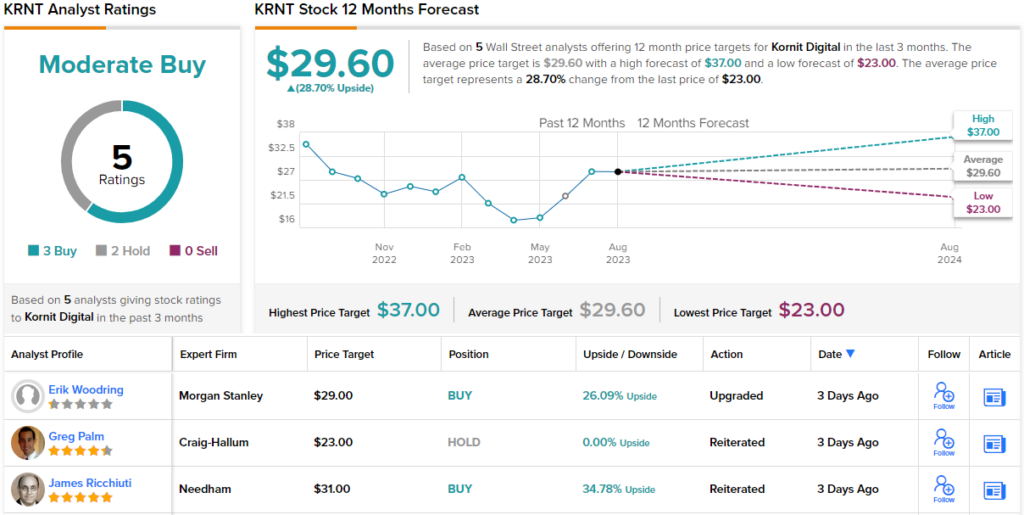

This upgrade to Overweight is accompanied with a $29 target price, which indicates confidence in a 26% gain on the 12-month horizon. (To watch Woodring’s track record, clickhere)

Looking at the overall picture, we see that Kornit received 5 recent reviews with 3 Buys, 2 Holds, and a Moderately Buy consensus. The shares are currently trading at $23 with an average price target of $29.60. This represents a 29% rise from the current level. (See Stock forecast for Kornit)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: This article is solely the opinion of the analysts featured. This content is only intended for informational use. You should always do your own research before investing.